NEW PROPOSED AMENDMENT TO THE TAXATION FOR SA TRUSTS’ WITH NON-RESIDENT BENEFICIARIES -DRAFT TAXATION LAWS AMENDMENT BILL, 2023

By Sean Eastman

August 2023

With more and more wealthy South African families seeking greener pastures abroad, it has become increasingly important to ensure that your estate planning is set up properly to prevent unnecessary tax surprises in future. As you might know, when a beneficiary of a SA discretionary trust moves abroad and ceases his/her SA tax residency it could become problematic out of a tax and estate planning perspective. Combine that with a new jurisdiction and you could have the perfect storm without proper planning.

On the 31st of July 2023, Treasury, and the South African Revenue Service (SARS) published for public comment the 2023 draft Taxation Laws Amendment Bill (2023 draft TLAB).

Conduit Principle - What is the proposed amendment?

Generally, where a trust receives an amount which it distributes to a beneficiary, the amount in question can retain its character in (and be taxed in) the hands of the recipient beneficiary. In legal terms the trust has acted as a mere conduit, rather than as an intermediate taxpayer, with the result that the amount has passed through the trust without being taxed and has retained its character (as income or capital or as exempt income, dividends, interest, etc.) when received by the beneficiary.

Paragraph 80 of the Eighth Schedule to the Act refers to a trust determining a capital gain, which must then be disregarded by such trust and taken into account by the resident beneficiary in whom the asset vests. Section 25B of the Act does not have a limitation on who the beneficiaries of a South African trust may be, so could therefore be residents or non-residents.

It is therefore accordingly proposed that changes be made to section 25B of the Act to align it with the provisions of paragraph 80 of the Eighth Schedule to the Act by limiting the flow through principle only to resident beneficiaries.

what does this mean in layman's terms?

Currently, when a SA trust makes a Capital Gain or earns income (interest for example) and Section 7 does not apply, the trust can use the conduit principle and distribute this gain and income to a resident beneficiary. Main reason for doing this is because the CGT rate for a SA trust is 36% compared to a maximum effective rate of 18% for individuals and the income tax rate of a trust is 45% where an individual can fall in a lower bracket depending on their total income earned (between 18%-45%).

However, for purposes of a capital gain the conduit principle does not extend to Non-resident beneficiaries as set out in paragraph 80 of the 8th Schedule to the Act. In short, the trust will be liable for CGT at 36% if it vests a capital gain in a non-resident beneficiary.

The income tax provision of this is set out in Section 25B of the Act which mirrors the capital gain provision as set out in paragraph 80, but with one significant difference – the conduit principle still applies to non-resident beneficiaries who receives an income distribution from the trust.

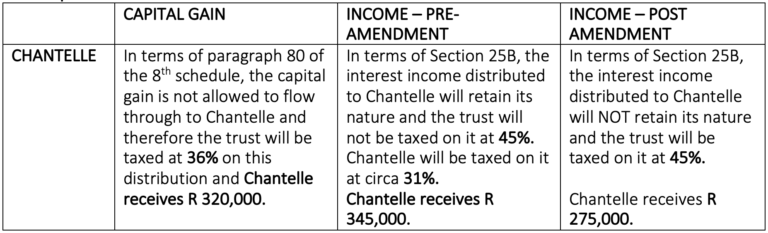

In the example below, see the economical effect of this amendment on distributions made to a non-resident beneficiary – Chantelle is a non-resident and beneficiary of a SA trust. In the 2023 financial year and 2024 (post-amendment) financial year she receives the following distributions (assume Section 7 does not apply)

Capital Gain of R 500,000 and Income of R 500,000.

APPLICATION OF THE CONDUIT PRINCIPLE

conclusion

The proposed amendments are deemed to have come into operation on 31 July 2023 and applies in respect of any years of assessment ending on or after the date. The feasibility of using SA trusts for purposes of your family’s Estate Planning is decreasing significantly and perhaps a good time to revisit your current structures to see if it is still relevant and tax efficient.

Given the relaxation by SARB of loop structures, SA residents can set up an offshore trust in a low tax jurisdiction to hold his/her worldwide assets including SA assets. This provides you with global exposure and long-term wealth protection. Whether you are currently looking at setting up a trust structure in SA or already have a SA family trust, it is not all bad news and there are still various methods to restructure this to ensure longevity, wealth protection and tax efficiency.

If you have any queries or would like to discuss this in more detail, please feel free to contact me on 082 773 5488 or email me at shaun@seconsulting.co.za.